Credit Union vs Bank Mortgages: Member Benefits with Rates & Terms

The average mortgage borrower compares only 2–4 lenders before making one of the largest financial decisions of their life. On a $450,000 home loan in the DFW area—close to the median price in Roanoke or Grapevine—a 0.50% difference in interest rate adds up to more than $75,000 in extra interest paid over 30 years. That’s not a rounding error. That’s a car, a college fund, or years of retirement savings. If you’re trying to figure out whether a credit union or a bank will give you a better deal on your mortgage, you’re asking exactly the right question—and the honest answer is more nuanced than the marketing from either side would have you believe.

This guide breaks down the real differences between credit union and bank mortgages in the DFW market—rates, fees, product availability, regulatory protections, and which lender type actually fits different borrower situations. No hype, no generic advice. Just the data and context you need to make a confident decision.

Key Takeaways

- Credit unions are not-for-profit and member-owned; banks are for-profit and shareholder-driven. This structural difference shapes everything from rates to service style—but doesn’t automatically make one better than the other.

- In 2026, large banks often match or beat credit union rates on conforming loans. The “credit unions always have lower rates” assumption is not reliably true.

- Rate differences of even 0.25% on a $450,000 DFW loan translate to tens of thousands of dollars over 30 years—making comparison shopping financially critical, not optional.

- Credit unions excel at personalized service and member benefits; banks lead on product variety, jumbo loans, and digital speed.

- Both lender types are heavily regulated, NMLS-licensed, and federally insured—your consumer protections are strong regardless of which you choose.

- The best lender for you depends on your financial profile, priorities, and the specific loan type you need—not on blanket assumptions about either institution type.

- DFW-specific factors like Tarrant and Denton County property taxes, HOA fees in master-planned communities, and the active new construction market in Trophy Club and Roanoke all influence which lender type may serve you better.

Why the Credit Union vs. Bank Decision Matters in the 2026 DFW Market

The Dallas-Fort Worth metro is one of the most competitive mortgage markets in the country. With roughly 7.9 million residents and consistent population growth driven by corporate relocations and job creation, DFW generates enormous demand for home financing—and lenders know it. In Trophy Club, Grapevine, Roanoke, Southlake, and Keller, median home prices range from $480,000 to well over $650,000, and median household incomes run from $95,000 in Grapevine to $168,000 in Trophy Club. These are not entry-level markets. Buyers here are often financing $400,000–$700,000 homes, which means the difference between a good rate and a great rate has real financial weight.

Banks currently hold 60–70% of Texas mortgage origination volume. Independent mortgage companies hold another 15–25%. Credit unions account for roughly 5–10% of originations—a smaller share, but a growing one, particularly among borrowers who value personalized service and member-focused pricing. The point isn’t that one type dominates; it’s that you have real options, and those options have meaningful differences in how they price loans, structure fees, and handle your application.

Rate differences between lender types can be negligible on any given day—or they can be significant, depending on your credit profile, loan type, down payment, and the specific institution. That variability is exactly why comparing multiple lenders isn’t just smart—it’s financially necessary. If you’re ready to start exploring your options, you can apply for a mortgage in DFW and see how different lender types stack up for your specific situation.

You’re Right to Compare—It Matters

The average borrower compares only 2–4 lenders, yet a 0.50% rate difference on a $450,000 loan costs over $75,000 in extra interest over 30 years. Your instinct to shop around isn’t just due diligence—it’s one of the most financially impactful decisions you’ll make in the entire home buying process.

Credit Union Mortgages: How Member-Owned Lending Works

Credit unions operate on a fundamentally different business model than banks. They are not-for-profit, member-owned cooperatives—which means instead of returning profits to shareholders, they return value to members through better rates, lower fees, or member dividends. That structural difference is real and meaningful, but it doesn’t automatically translate into a better mortgage for every borrower in every situation.

Several DFW-area credit unions are active mortgage lenders with broad community charters, meaning you don’t need to work for a specific employer to join. RBFCU (NMLS# 445727) is well-known across Texas for competitive rates and member-focused service. Amplify Credit Union (NMLS# 470654) has an expanding footprint. TDECU (NMLS# 598705) serves a broad field of membership. EECU (NMLS# 405156) is Fort Worth-based and serves educators and community members throughout North Texas. Navy Federal Credit Union (NMLS# 482761), the largest credit union in the world, serves military personnel and DOD employees and their families—a significant population in the DFW corridor.

When you work with any of these lenders, it’s worth taking a moment to understand key mortgage terminology so you can evaluate their offers with confidence. And always verify a lender’s credentials at nmlsconsumeraccess.org before moving forward.

Membership Requirements and Accessibility

One of the most common misconceptions about credit unions is that they’re hard to join. For most DFW-area credit unions, that’s simply not true. Community charters mean that if you live, work, or worship in the DFW metro area, you likely qualify for membership. The process typically involves opening a share savings account—the credit union equivalent of a basic membership account—with a minimum deposit of just $5 to $25. That’s it. You can often complete the process online in minutes or walk into a branch and be a member the same day.

Once you’re a member, you’re eligible for member rates, relationship pricing, and any benefit programs the credit union offers. The barrier to entry is genuinely low, which means there’s little reason not to at least get a quote from a credit union when you’re shopping for a mortgage.

Credit Union Mortgage Products and Flexibility

Credit unions offer a solid range of standard mortgage products. Conforming 30-year and 15-year fixed loans, FHA loans, VA loans, and USDA loans are all competitively available through most DFW credit unions. Where credit unions can fall short is in the niche and specialty product categories. Jumbo loans—relevant for buyers in Trophy Club where median prices exceed $650,000—are sometimes available through credit union partnerships rather than direct origination, which can mean higher rates or less flexible terms. Construction-to-permanent loans and renovation financing exist at many credit unions but with fewer product variations than you’d find at a large bank.

Credit unions also tend to have more personalized underwriting processes. For borrowers with slightly non-traditional financial profiles—self-employed income, recent job changes, or unique asset structures—a credit union’s willingness to look at the full picture of your membership history and financial relationship can be an advantage. That said, this isn’t a guarantee of approval; credit unions still follow conforming guidelines for the loans they intend to sell on the secondary market.

Bank Mortgages: Scale, Product Variety, and Automation

Banks operate on a for-profit model with a heavy focus on the secondary market—meaning they originate loans and sell them to Freddie Mac and Fannie Mae. That secondary market orientation drives standardized products, competitive pricing at scale, and sophisticated technology platforms. It also means your loan is more likely to be sold to a different servicer after closing, which is worth understanding before you commit.

Major DFW bank mortgage lenders include JPMorgan Chase (NMLS# 399700), Wells Fargo (NMLS# 399801), Bank of America (NMLS# 124771), Truist Bank (NMLS# 635537), Frost Bank (NMLS# 557615), and Prosperity Bank (NMLS# 466541). Frost Bank and Prosperity Bank are Texas-based community banks with strong regional reputations and more personalized service than their national counterparts—worth considering if you want bank product variety with a more relationship-focused experience.

Bank of America’s Preferred Rewards program offers rate discounts and fee reductions for customers with significant existing balances across their accounts. If you already have substantial assets with a bank, those relationship benefits can be meaningful—sometimes comparable to what a credit union member discount would offer. When you’re ready to compare mortgage offers from multiple lenders, factoring in these relationship discounts is an important step most borrowers overlook.

Bank Product Range and Specialization

The product breadth at large banks is genuinely hard to match. Jumbo loans for Trophy Club or Grapevine properties priced above the 2026 conforming loan limit (approximately $806,500 based on FHFA trends) are readily available with competitive rates at large banks that have the capital reserves and secondary market access to fund them efficiently. Doctor and dentist loan programs—which allow high-income professionals to purchase with minimal down payment and no PMI—are almost exclusively a bank product. Investment property financing, portfolio loans for self-employed borrowers, and construction-to-permanent loans for the active new-build market along SH-114 are all areas where banks have significantly more depth than credit unions.

Digital Experience and Speed

If you value a streamlined digital experience—uploading documents from your phone, tracking your loan status in real time, and potentially closing electronically—large banks have invested heavily in these capabilities. Automation speeds up initial processing and reduces friction in the early stages of the application. For standard conforming loans, large banks average 45–60 days to close, with e-closing capabilities increasingly standard. That said, automation isn’t a substitute for a responsive loan officer when your file hits a snag—and that’s where some large banks draw criticism in CFPB complaint data.

Ready to explore your options? Comparing offers from credit unions, banks, and independent lenders side by side is the most effective way to find the best combination of rate, fees, and service for your DFW home purchase.

Start Your Mortgage ComparisonRates, Fees, and True Cost Comparison

This is where most borrowers get tripped up—and where the marketing from both credit unions and banks can be misleading. Let’s work through the actual numbers.

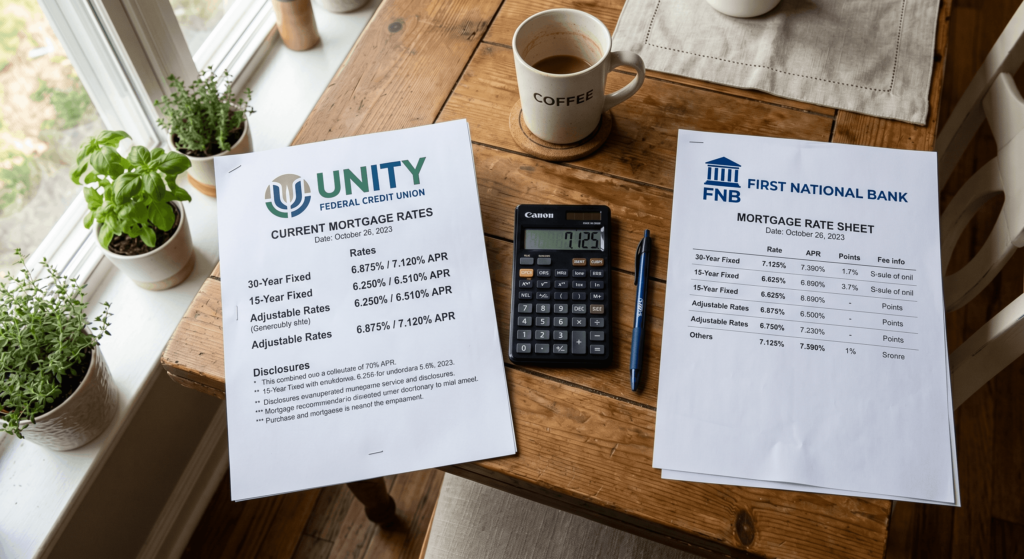

In 2026, the rate differential between credit unions and banks on conforming loans is often negligible—typically 0.05% to 0.15% in either direction, depending on the day, your credit profile, your loan-to-value ratio, and the specific institution. Some credit unions advertise slightly lower “best case” rates or member discounts, but large banks compete aggressively on conforming loan rates due to their secondary market scale. The assumption that credit unions automatically offer better rates is not reliably true in the current market.

What matters more than the advertised rate is the total cost of the loan. On a $450,000 mortgage, here’s a realistic fee comparison:

- Credit union lender fees: Estimated $3,000–$6,000 (often lower or partially waived for members)

- Bank lender fees: Estimated $4,000–$7,000 (negotiable, especially for preferred customers)

- Independent mortgage company fees: Estimated $3,500–$6,500 (often most aggressive on fees to compete on price)

Total closing costs—including appraisal, title insurance, escrow setup, prepaid items, and lender fees—typically run 2–5% of the loan amount regardless of lender type. The specific line items vary, but the total range is comparable. The biggest financial lever remains the interest rate itself. A 0.25% rate difference on a $450,000 loan over 30 years amounts to tens of thousands of dollars. That’s why getting a current rate comparison for DFW borrowers is worth the time it takes.

Pro Tip: The Rate Isn’t Everything

While interest rate is the primary cost driver, don’t overlook origination fees, appraisal costs, and lender reputation. A slightly higher rate from a responsive, reliable lender can be worth it if it means fewer delays, better communication, and a smoother closing. A chaotic closing process in a competitive DFW market can cost you the house—not just money.

2026 Rate Environment for DFW Borrowers

The DFW mortgage market in 2026 remains predominantly purchase-focused, with refinance activity still suppressed compared to the historically low-rate era of 2020–2021. Both credit unions and banks are competing aggressively for purchase volume, which is actually good news for buyers—it creates genuine pricing competition. On 30-year fixed conforming loans, credit unions sometimes offer 0.125%–0.25% lower rates or member discounts, but this advantage isn’t consistent across all institutions or all days. For jumbo loans—relevant for Trophy Club buyers financing above the conforming limit—large banks typically have the edge due to their capital reserves and secondary market relationships. FHA and VA loan rates are generally competitive across both credit unions and banks, with credit unions sometimes offering more flexible underwriting for members who have a demonstrated financial relationship.

Fee Breakdown and Negotiation Potential

Origination fees are the largest controllable cost in your closing costs, and they’re negotiable at every lender type—though the approach differs. Credit unions may be more willing to reduce or waive origination fees for members, particularly those with checking accounts, direct deposit, or other products at the institution. Banks may have more standardized rate sheets, but preferred customer programs can provide meaningful fee reductions. One often-overlooked cost difference involves rate lock policies: credit unions may offer shorter or less flexible rate lock periods, which can create risk if your closing is delayed. Always ask specifically about rate lock duration, extension fees, and what happens if rates drop during your lock period. To get a Loan Estimate to compare true costs, you’ll want to request one from at least three lenders—credit union, bank, and independent mortgage company—within the same 45-day window.

Regulatory Oversight: NMLS, NCUA, OCC, and Consumer Protections

One of the most reassuring aspects of the mortgage market—regardless of whether you choose a credit union or a bank—is that both are heavily regulated. The consumer protection framework is robust, and understanding it gives you real leverage as a borrower.

Every mortgage loan originator (MLO) in Texas must be licensed through the Nationwide Multistate Licensing System & Registry (NMLS). This license requires passing education requirements, a national exam, a state exam, a background check, and ongoing continuing education. You can verify any lender or loan officer at nmlsconsumeraccess.org—a free, public database. This is not optional due diligence; it’s a 60-second check that confirms you’re working with a legitimate, regulated professional.

Federal credit unions are regulated by the National Credit Union Administration (NCUA), which focuses on member safety and soundness. Federally chartered banks fall under the Office of the Comptroller of the Currency (OCC). State-chartered institutions—both banks and credit unions—are regulated by the Texas Department of Savings and Mortgage Lending (TDSMLS). Deposits at banks are insured by the FDIC; deposits at credit unions are insured by the NCUA up to $250,000. Both are federally backed. Both are required to maintain capital reserves, fidelity bonds, and errors and omissions (E&O) insurance.

The Consumer Financial Protection Bureau (CFPB) has broad oversight over both institution types, enforcing critical consumer protection laws including TRID (which governs the Loan Estimate and Closing Disclosure forms), RESPA, and ECOA. If you want to understand mortgage disclosure requirements and what each form means for your transaction, familiarizing yourself with these terms before you start shopping will make you a more informed borrower.

What NMLS License Verification Really Means

An NMLS license confirms that a loan officer has passed education, examination, and background check requirements. Verifying at nmlsconsumeraccess.org ensures you’re working with a legitimate, regulated professional. It’s a baseline of legitimacy—not a guarantee of quality—but it’s a critical first step before trusting anyone with your mortgage application.

How to Verify Lender Credentials

The process is simple: go to nmlsconsumeraccess.org and search by company name or the individual loan officer’s name or license number. Check the license status—it should read “Active”—and review any history of disciplinary actions. If a lender’s NMLS number doesn’t match what’s on their official marketing materials or loan documents, that’s a red flag worth investigating before proceeding.

2025–2026 Regulatory Trends Affecting DFW Borrowers

The CFPB continues to update mortgage lending rules with a focus on expanding affordable mortgage access for lower-to-moderate income borrowers, enhancing servicing protections for borrowers facing financial hardship, and reforming appraisal processes to improve accuracy and reduce bias. Texas legislative sessions may also introduce state-specific changes to lending disclosures or practices. If you have a complaint against any lender, your recourse options include the CFPB (federal consumer protection), TDSMLS (Texas-specific violations), NCUA (federal credit union issues), and the Texas DTPA for broader contractual or deceptive practice claims.

Understanding your options is the first step. Get a personalized Loan Estimate to see how credit union and bank rates compare for your specific financial situation and DFW home purchase.

Get Your Personalized Loan EstimateHead-to-Head Comparison: Which Lender Type Wins for Different Borrower Profiles

The honest answer to “credit union vs. bank” is that it depends on who you are and what you need. There’s no universal winner. What there is, however, is a clear framework for matching lender type to borrower profile—and that’s far more useful than a generic recommendation.

Credit unions tend to be the strongest fit for existing members who can leverage relationship pricing, borrowers who value personalized service over digital automation, and those with slightly non-conventional financial profiles who benefit from more individualized underwriting consideration. If you’re already a member of RBFCU or EECU and have a checking account there, requesting a quote from your credit union should be your first call—the member discount alone can be meaningful.

Banks are typically the better choice for borrowers who need jumbo financing, niche loan products (doctor loans, investment property, construction-to-permanent), or who want the fastest and most technologically seamless experience. Existing bank customers with significant assets should specifically ask about preferred customer programs—these can provide rate or fee discounts that rival credit union member benefits.

Independent mortgage companies occupy a different space: they’re typically the most aggressive on rate and fee pricing, often closing faster than either credit unions or banks, but with less of a relationship component. For price-sensitive borrowers who are comfortable navigating the process independently, they’re worth including in your comparison. You can explore the full range of mortgage loan options available in DFW to understand which products align with your situation before you start requesting quotes.

Best for First-Time Homebuyers in DFW

First-time buyers in markets like Keller, Argyle, or Colleyville face a specific set of challenges: navigating the process for the first time, managing down payment resources, and often qualifying with less established credit histories. Credit unions can offer a more guided, personalized experience—a loan officer who knows your name and has time to walk you through the process is genuinely valuable when you’re doing this for the first time. Banks provide robust educational resources, wide product menus including FHA and down payment assistance programs, and digital tools that make document management easier. The most important thing for first-time buyers isn’t choosing between credit union and bank—it’s comparing Loan Estimates from both, plus at least one independent lender, to see which combination of rate, fees, and service fits your situation.

Best for Jumbo Loan Seekers in Trophy Club, Grapevine, and Roanoke

With Trophy Club median home prices exceeding $650,000 and premium properties in Grapevine and Southlake regularly pushing well above the conforming loan limit, jumbo financing is a real consideration for many DFW buyers. Large banks dominate this space. Their capital reserves, secondary market relationships, and institutional infrastructure for jumbo underwriting give them a structural advantage. Credit unions may offer jumbo loans through partnerships, but rates and terms are often less competitive. If you’re financing a high-value property, banks should be your primary focus—though it’s still worth asking your credit union for a quote to confirm the comparison.

Best for Speed and Automation

In a competitive DFW market where sellers sometimes receive multiple offers, closing speed matters. Large banks average 45–60 days to close on standard conforming loans, with sophisticated technology reducing friction in the early stages. Independent mortgage companies often close in 35–50 days and frequently prioritize speed as a competitive differentiator. Credit unions are improving—many now average 40–55 days—but their more personalized underwriting process can add time for complex files. If speed is your primary concern, ask each lender for their average days-to-close on a loan like yours, and ask specifically what factors could cause delays. To start comparing mortgage offers today, getting pre-approved with multiple lenders simultaneously is the most efficient approach.

Dispelling Common Myths: What the Data Actually Shows

A lot of conventional wisdom about credit union vs. bank mortgages doesn’t hold up when you look at actual data. Here are the five myths worth addressing directly.

Myth: “Credit unions always have lower rates than banks.”

Reality: In 2025 and into 2026, large banks have frequently matched or beaten credit union rates on conforming loans, driven by their secondary market scale and aggressive competition for purchase volume. Rate competitiveness varies daily and depends on loan type, credit profile, LTV, and the specific institution. The only way to know which is cheaper for you is to request actual Loan Estimates from both.

Myth: “Banks have more complaints because they’re worse lenders.”

Reality: Banks receive higher complaint volumes in CFPB data primarily because they originate 60–70% of all mortgages. When you analyze complaint rates per loan volume, some large banks have comparable or higher per-loan complaint rates than credit unions—but this isn’t universal. Common complaints for both types include servicing issues (escrow management, payment processing) and origination delays. The complaint data reflects scale, not necessarily quality.

Watch Out: The ‘Always Lower’ Myth

Credit unions don’t automatically have lower rates than banks. In 2025 and 2026, large banks have frequently matched or beaten credit union rates on conforming loans. Always request Loan Estimates from both types—and from at least one independent lender—before making any assumptions about who offers the better deal.

Myth: “Credit unions are always more flexible on underwriting.”

Reality: Credit unions may offer more personalized consideration for members with unique financial situations, but they’re still bound by conforming guidelines for loans they intend to sell on the secondary market. They may actually be less likely to approve marginal applications that fall outside strict guidelines than a bank with a robust portfolio loan program. Flexibility depends heavily on the specific credit union and borrower profile.

Myth: “Your mortgage will definitely be sold to a different servicer.”

Reality: Larger credit unions often service their own mortgages in-house, which means your loan stays with the institution you chose. Banks are more likely to sell loans on the secondary market, but servicing transfers are legal, regulated, and subject to CFPB notification requirements. If keeping your loan with the same institution matters to you, ask any lender upfront whether they service their own loans—it’s a fair and important question.

Myth: “You can’t negotiate rates and fees with credit unions.”

Reality: Negotiation is possible with all lender types. Credit unions may actually be more open to relationship pricing discussions—particularly for members with multiple products at the institution. Banks may have more rigid rate sheets but can sometimes be flexible on specific fees. Independent mortgage companies often have the most direct authority to negotiate. Don’t assume the first offer is final at any lender. To verify actual numbers, request Loan Estimates from multiple lenders and use them as negotiating tools.

Key Statistics: Market Share, Denial Rates, and Days-to-Close

Data gives this comparison real grounding. Here’s what the numbers actually show about how credit unions and banks perform on the metrics that matter most to borrowers.

Market share in Texas: Banks dominate with 60–70% of mortgage origination volume. Independent mortgage companies hold 15–25%. Credit unions account for approximately 5–10%, though their share has been growing steadily as more borrowers discover their member benefits and competitive pricing. (Source: Mortgage Bankers Association, TDSMLS annual reports)

Denial rates: Credit unions historically have had slightly lower denial rates for mortgage applications compared to banks. This is often attributed to their member-centric underwriting approach and the advantage of knowing a borrower’s full financial history through their existing relationship. However, this advantage is most pronounced for existing members—not new applicants joining specifically to get a mortgage. (Source: CFPB data analysis)

Days-to-close averages: Large banks average 45–60 days. Credit unions average 40–55 days (improving with technology investment). Independent lenders average 35–50 days, often prioritizing speed as a competitive differentiator. These are industry averages—individual lender performance varies significantly based on loan complexity and operational efficiency. (Source: ICE Mortgage Technology)

The cost of not shopping: The average borrower compares only 2–4 lenders. On a $450,000 DFW loan, a 0.50% rate difference over 30 years costs over $75,000 in additional interest. Even a 0.25% difference translates to tens of thousands of dollars. The financial case for comparing multiple lender types is overwhelming. If you’re ready to take that step, explore mortgage options in DFW with a lender who understands the local market dynamics.

Consumer decision drivers: According to consumer lending surveys and NAR buyer behavior studies, the primary factors borrowers consider when choosing a mortgage lender are: interest rate (primary), fees, loan product availability, lender reputation and service quality, and ease of the application process. Rate is dominant—but it’s not the only variable that matters, and the borrowers who focus exclusively on rate sometimes end up with a worse overall experience.

Texas-Specific Factors That Impact Your Mortgage Choice

The DFW market has characteristics that don’t show up in national mortgage comparisons—and they matter for how you evaluate credit union vs. bank offers specifically in this area.

Property taxes in Tarrant County and Denton County are relatively high compared to national averages, and they have a significant impact on your monthly PITI (Principal, Interest, Taxes, Insurance) payment. A buyer financing a $550,000 home in Trophy Club isn’t just managing a mortgage payment—they’re also managing a substantial annual property tax bill that gets escrowed monthly. Lenders factor property taxes into debt-to-income ratio calculations, which can affect your loan approval amount in ways that borrowers from lower-tax states find surprising. Understanding how DFW property taxes affect your mortgage approval is an important step before you start shopping lenders.

DFW-Specific Insight: Property Taxes Impact Your Approval

Tarrant and Denton County property taxes are relatively high and significantly impact your monthly PITI payment. Lenders factor these into debt-to-income calculations, which can affect your loan approval amount. Don’t overlook this when comparing offers—a lender who understands local tax rates will give you a more accurate pre-approval than one using national averages.

Master-planned communities like Trophy Club also carry substantial HOA fees—sometimes $200–$500 per month or more—which lenders must include in debt-to-income calculations. This further compresses the loan amount some buyers can qualify for, making it even more important to work with a lender who understands the local market and factors these costs in accurately from the start.

Texas homestead exemptions provide some property tax relief, which can slightly reduce monthly escrow payments over time. This applies regardless of lender type, but it’s worth understanding when you’re projecting long-term housing costs.

Texas Constitution Article XVI, Section 50(a)(6) places specific limitations on home equity loans and certain cash-out refinance terms—protections that are unique to Texas and designed to prevent borrowers from being stripped of their home equity. Both banks and credit unions must adhere to these restrictions, and any lender operating in Texas should be well-versed in them. If a lender seems unfamiliar with Texas-specific homestead and equity rules, that’s a red flag worth noting.

New Construction and Construction Financing in DFW

The active new construction market along SH-114 and within Trophy Club, Roanoke, and Argyle creates significant demand for construction-to-permanent loans and end-financing products. Banks typically offer more robust construction financing options—more product variations, more flexible draw schedules, and more experience with the builder relationships common in DFW’s master-planned communities. Credit unions may offer construction loans but often with fewer product variations and potentially less experience with the specific builders and communities in the area. If you’re buying new construction, banks should be your primary focus for construction financing, though you should still compare end-loan rates from credit unions once the home is complete.

Property Taxes and Affordability in DFW Suburbs

To put the property tax impact in concrete terms: a $600,000 home in Trophy Club might carry an annual property tax bill of $12,000–$15,000, adding $1,000–$1,250 per month to your escrow payment on top of principal, interest, and insurance. That total PITI can significantly affect your debt-to-income ratio and the loan amount you qualify for. Texas homestead exemptions reduce the taxable value of your primary residence, which provides some relief—but the base tax rates in these counties are still among the highest in the state. Any lender quoting you a payment without accurately accounting for local property taxes is giving you an incomplete picture.

How to Compare Credit Union and Bank Mortgage Offers: A Step-by-Step Guide

Knowing the differences between credit unions and banks is only useful if you translate that knowledge into action. Here’s how to actually run the comparison in a way that gives you reliable, apples-to-apples data.

Step 1: Request Loan Estimates from at least 3 lenders simultaneously. Include at least one credit union, one bank, and one independent mortgage company. Do this within a 45-day window—multiple credit inquiries for mortgage purposes within that window are treated as a single inquiry by the major credit bureaus, minimizing the impact on your credit score.

Step 2: Compare the Loan Estimate form line by line. The Loan Estimate is a standardized federal form—every lender uses the same format, which makes direct comparison straightforward. Focus on: interest rate, APR (which includes fees and gives a more complete cost picture), origination fees, appraisal fees, title insurance, escrow setup, and total estimated cash to close. Make sure you’re comparing the same loan type (e.g., 30-year fixed conforming) across all lenders.

Step 3: Ask about rate lock policies. Specifically: How long is the rate lock? (Typically 30–60 days.) What are the extension fees if closing is delayed? Is there a float-down option if rates drop during the lock period? Credit unions and banks handle these differently, and the answers can affect your total cost if your closing timeline shifts.

Step 4: Ask about member benefits and relationship pricing. For credit unions: Do you offer rate or fee discounts for members with checking accounts or direct deposit? For banks: Do you have a preferred customer program, and what are the eligibility requirements? These discounts can sometimes be significant and aren’t always advertised upfront.

Step 5: Verify NMLS licenses. Every loan officer and lending institution should have an active NMLS license. Check nmlsconsumeraccess.org before you submit a full application anywhere. Look for active status and no significant disciplinary history.

Step 6: Ask about days-to-close and potential delays. Get a realistic estimate from each lender, and ask what factors could cause delays specific to your loan type. For DFW new construction, ask about their experience with builder timelines and construction loan draws.

Step 7: Check reviews and references. Google reviews, Trustpilot, and the Better Business Bureau can reveal patterns in customer service quality and follow-through. One or two negative reviews are normal; a consistent pattern of communication failures or closing delays is a meaningful signal.

Step 8: Don’t make the decision on rate alone. The total cost—rate plus fees—matters. So does the lender’s track record for communication, responsiveness, and delivering on their timeline commitments. In a competitive DFW market, a lender who drops the ball on your closing can cost you the house. To get your Loan Estimate from a DFW mortgage lender who understands the local market, the process is straightforward and there’s no obligation to proceed.

Understanding the Loan Estimate Form

The Loan Estimate is one of the most powerful consumer protection tools in the mortgage process. It’s a standardized three-page form that every lender is required to provide within three business days of receiving your application. Page 1 shows the loan terms, projected monthly payment, and estimated closing costs. Page 2 breaks down every closing cost in detail—which ones are fixed, which can change, and which you can shop for independently. Page 3 shows comparisons and contact information. When you have Loan Estimates from three lenders side by side, the differences become immediately visible—and that visibility is what gives you negotiating power.

Questions to Ask Each Lender Before Committing

- What is your rate lock policy, and are there extension fees if closing is delayed?

- Do you offer any member benefits, relationship pricing, or discounts for existing customers?

- What is your estimated days-to-close for a loan like mine, and what factors could delay the process?

- Will you service this loan in-house, or will it be sold on the secondary market?

- Are there any prepayment penalties or other restrictions on this loan product?

- How do you handle appraisal issues or underwriting conditions that could affect the closing timeline?

Start comparing offers today and see which lender type offers the best combination of rate, fees, and service for your DFW home purchase. The comparison takes less time than you think—and the savings can be substantial.

Compare Your Mortgage Options NowFrequently Asked Questions: Credit Union vs. Bank Mortgages

What’s the real difference in mortgage rates between credit unions and banks?

The honest answer is: it depends on the day, the loan type, and your specific financial profile. Historically, credit unions sometimes offered slightly lower rates or fees due to their non-profit structure—and that advantage still exists in some situations, particularly for existing members who qualify for relationship pricing. However, in 2025 and 2026, large banks have frequently matched or beaten credit union rates on conforming loans because of their secondary market scale and aggressive competition for purchase volume. Rate differences between the two are often in the 0.05%–0.15% range—negligible in some cases, meaningful in others. The only reliable way to know which is cheaper for your specific situation is to request actual Loan Estimates from both types and compare the numbers side by side.

How easy is it to get a mortgage at a credit union if I’m not already a member?

For most DFW-area credit unions, it’s genuinely easy. The majority have broad community charters, meaning you qualify for membership simply by living or working in the DFW metro area—you don’t need to work for a specific employer or belong to a specific group. The process typically involves opening a share savings account with a minimum deposit of $5 to $25, which immediately qualifies you for member rates and benefits. You can often complete this online in minutes or walk into a branch and be a member the same day. There’s no meaningful barrier to at least getting a quote from a credit union as part of your lender comparison.

Do credit unions offer the same mortgage products as banks, like jumbo loans or renovation loans?

Credit unions offer standard mortgage products—conforming 30-year and 15-year fixed loans, FHA, VA, and USDA loans—very competitively, and these products are well-suited for the majority of DFW home purchases. Where credit unions fall short is in niche and specialty products. Jumbo loans for high-value properties in Trophy Club or Southlake may be available through credit union partnerships rather than direct origination, which can mean less competitive rates or terms. Specialized renovation loans, construction-to-permanent financing, doctor/dentist loans, and investment property products are areas where large banks have significantly more depth and flexibility. If your purchase requires a niche product, banks should be your primary focus—though it’s still worth asking your credit union what they offer before assuming.

What happens if my credit union mortgage application is delayed or my rate lock expires?

Delays can happen with any lender type—credit union, bank, or independent mortgage company. The key is understanding the rate lock policy before you apply, not after you’re in the middle of a transaction. Ask specifically: How long is the rate lock period? What are the extension fees if closing is delayed beyond that window? Is there a float-down option if rates drop? Some credit unions may offer more flexibility on extensions due to their member-focused approach, but this varies by institution and isn’t guaranteed. In the DFW market, where appraisal issues and title complications can arise unexpectedly, having a clear understanding of your rate lock terms is essential regardless of which lender type you choose.

Are credit union mortgage lenders more flexible on underwriting if I have a checking account there?

Having an established relationship with a credit union can be beneficial, but it doesn’t automatically guarantee more flexible underwriting or loan approval. The advantage is more nuanced: credit unions may have a better understanding of your financial history through your existing accounts, and a loan officer who knows your situation may advocate for your file more effectively than an automated underwriting system would. For borderline applications—where income documentation is complex, credit history has a few blemishes, or assets are structured unusually—that personal familiarity can make a real difference. For straightforward applications that clearly meet conforming guidelines, the difference is less significant. The relationship benefit is real but situational.

Which type of lender is best for a first-time homebuyer in DFW: credit union, bank, or independent mortgage company?

There’s no single right answer—which is actually the most important thing to understand. Credit unions offer personalized guidance and potential member benefits that can be genuinely valuable for first-time buyers navigating an unfamiliar process. Banks provide robust digital tools, wide product menus including FHA and down payment assistance programs, and educational resources. Independent mortgage companies often focus on competitive pricing and speed, which matters in a fast-moving DFW market. The most important step for any first-time buyer isn’t choosing between these types—it’s comparing Loan Estimates from all three to see which combination of rate, fees, service quality, and communication style fits your specific situation and comfort level. You can also ask a mortgage professional to help you evaluate your options without any pressure to commit.

Ready to Compare Your Mortgage Options with Confidence?

Choosing between a credit union and a bank mortgage doesn’t have to be overwhelming—it just requires the right information and the right comparison. At Oasis Home Mortgage in Trophy Club, we work with buyers throughout the DFW area, including Grapevine, Roanoke, Southlake, Keller, Argyle, and Colleyville, to help them understand their options and find the loan that actually fits their situation.

There’s no pressure, no obligation—just a straightforward Loan Estimate that gives you real numbers to compare. That’s how confident decisions get made.

Get Your No-Obligation Loan EstimateOasis Home Mortgage | 7 Greenbriar Ct, Trophy Club, TX 76262