Mortgage Broker vs Bank Direct: Which Saves You More Money in 2026?

The average borrower who shops with only one lender pays $15,000–$20,000 more over the life of their loan than those who compare at least three options. And most borrowers have no idea that the difference between going to a mortgage broker versus a bank direct lender can add another $5,000–$10,000 to that gap. That’s not a rounding error. That’s a car. A college semester. A decade of vacations. And it all comes down to a decision most people make in about 20 minutes without fully understanding what they’re choosing.

This guide exists to fix that. Not with marketing language, not with a pitch for one channel over the other—but with the actual structural differences, real numbers, and clear guidance on when each option wins. By the time you finish reading, you’ll know exactly which lending channel fits your situation and how to make sure you’re not leaving money on the table.

Key Takeaways

- Mortgage brokers access wholesale lenders and can offer lower rates—but their compensation adds back to the cost, so the net result depends on the specific deal.

- Bank direct lenders are competitive for borrowers with excellent credit and existing relationships, but their pricing is less transparent.

- A 0.25% rate difference on a $400,000 loan costs $18,000 over 30 years—small differences compound into large dollars.

- Brokers almost always win for self-employed borrowers, real estate investors, and jumbo loan borrowers due to product access.

- Both channels close in 30–45 days on average—the “banks are faster” myth doesn’t hold up to data.

- The real winner is always the borrower who shops both channels and compares at least 3 Loan Estimates on the same day.

- DFW borrowers have robust options in both channels—and the competition in this market works in your favor.

Why the Mortgage Broker vs Bank Decision Matters More Than You Think

Most people choose their mortgage lender the same way they choose a dentist: they go to whoever they already know. If you have a Chase checking account, you call Chase. If your parents used Wells Fargo, you call Wells Fargo. It feels logical. It feels safe. But here’s the thing—this default decision is costing DFW borrowers thousands of dollars every year, and most of them never find out.

The lending channel you choose isn’t just a preference question. It affects your interest rate, your fees, the loan products available to you, and how smoothly your closing goes. These factors don’t just affect your monthly payment—they compound over 30 years. A difference of 0.25% on a $500,000 loan in Southlake or Westlake isn’t a minor inconvenience. It’s $22,500 over the life of the loan. A difference of 0.375% is $33,000. That’s real money, and it’s the kind of money that stays in your pocket or leaves it based entirely on this one decision.

The DFW market is actually one of the best places in the country to be a mortgage borrower right now. With 200+ licensed mortgage brokers and 50+ direct bank lenders operating across Tarrant and Denton counties, you have genuine leverage. Trophy Club, Grapevine, Roanoke, Keller, Argyle, Colleyville—these communities are served by multiple competing lenders who want your business. That competition is your advantage, but only if you know how to use it.

You’re right to be confused about which path to take. The mortgage industry doesn’t make this easy to understand—and frankly, it benefits from borrowers not comparing. The best first step is to apply for a mortgage with multiple lenders so you can see real numbers side by side, not marketing claims.

Most borrowers default to their bank without realizing they have another option. The mortgage industry doesn’t make it easy to compare channels, which is exactly why this decision matters so much financially. The fact that you’re researching this puts you ahead of the majority of borrowers who never ask the question at all.

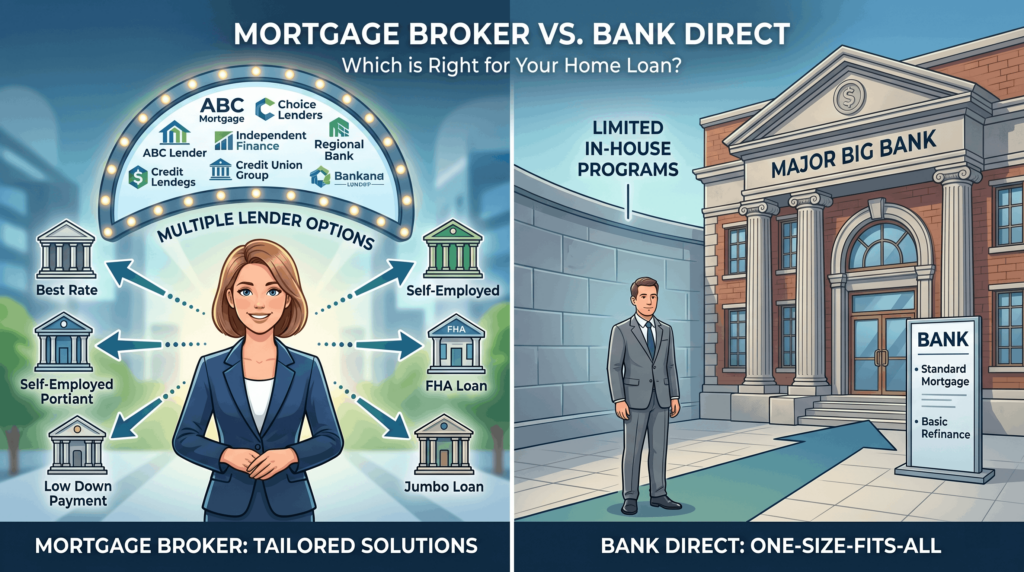

What Is a Mortgage Broker vs a Bank Direct Lender?

Before you can compare them, you need to understand what they actually are—not the marketing version, but the structural reality. These two types of lenders operate very differently, and those differences are what drive the pricing, product, and service gaps you’ll experience as a borrower.

Both mortgage brokers and bank loan officers must be NMLS-registered and comply with Texas state regulations. You can verify any lender’s credentials at nmlsconsumeraccess.org before you sign anything. Understanding mortgage licensing requirements in Texas helps you know who you’re working with and what protections apply to your transaction.

How Mortgage Brokers Work

A mortgage broker is an intermediary. They don’t lend their own money. Instead, they take your application and submit it to multiple wholesale lenders—often 50 to 100 or more—to find the best rate and terms for your specific situation. Think of them as a personal shopper for your mortgage. They have access to pricing that retail borrowers can’t get on their own, and they negotiate on your behalf.

Brokers are compensated in one of two ways: by the lender (through what’s called a yield spread premium, or YSP) or by the borrower (through a broker fee), or sometimes a combination. All compensation must be disclosed on your Loan Estimate within three business days of application—that’s a federal requirement. Brokers don’t hold your loan after closing. They facilitate the transaction and hand it off to the wholesale lender at closing.

The key advantage here is access. A broker working in the DFW market has relationships with dozens of wholesale lenders, each with different pricing models, risk appetites, and specialty products. That breadth is what creates the pricing advantage—and the product availability advantage—that brokers are known for.

How Bank Direct Lenders Work

A bank direct lender originates loans using the bank’s own capital or through correspondent relationships with other lenders. When you walk into Chase or Bank of America or Prosperity Bank, you’re working with a loan officer who is an employee of that institution. They can only offer you products that bank has approved—their own portfolio, plus any correspondent relationships they’ve established.

Bank loan officers are typically salaried with commission based on loan volume or margin. Their compensation is not disclosed to you as a borrower—it’s an internal bank matter. The bank may service your loan in-house after closing, or it may sell it on the secondary market. Either way, you’re working within that bank’s product menu, which is narrower than what a broker can access.

The key advantage for banks is the relationship. If you have existing deposits, investment accounts, or a long banking history, some banks will offer rate discounts or streamlined processing that brokers can’t match. For the right borrower profile, this relationship value is real.

Rate Comparison: Do Brokers Really Offer Better Pricing?

This is the question everyone wants answered, and the honest answer is: usually yes, but not always, and the gap varies significantly based on your credit profile, loan type, and the specific lenders involved.

Here’s the structural reality. Wholesale rates—the rates brokers access—are structurally lower than retail rates because wholesale lenders sell loans in bulk to investors. Lower volume risk per loan means lower pricing. Retail banks price higher because they carry more servicing risk and have higher overhead. That structural gap exists regardless of the market cycle.

But brokers don’t pass that wholesale rate directly to you. They add their compensation on top—typically 0.5% to 1.5% of the loan amount. So the net result depends on whether the broker’s compensation eats up the wholesale discount. On average, borrowers save 0.125% to 0.375% by working with a broker compared to a single bank. That range matters enormously when you do the math.

Wholesale vs Retail Pricing Explained

Wholesale lenders price their loans lower because they’re not dealing with individual retail borrowers—they’re working with brokers who deliver pre-packaged loan files in volume. That efficiency gets passed through as lower rates. Retail banks price higher because they’re managing the full customer relationship, maintaining branch infrastructure, and often holding more servicing risk.

A typical broker working in the DFW market might access wholesale pricing that’s 0.25% to 0.50% below what a retail bank quotes on the same loan. After the broker’s compensation (let’s say 1.0%), the net rate might be 0.125% to 0.25% better than the bank. That’s the typical broker advantage in a competitive market. But if the broker’s compensation is 1.5% and the wholesale discount is only 0.25%, the advantage disappears. This is why you compare total cost, not just rate.

To see today’s mortgage rates in Texas and understand how current pricing compares across loan types, checking a live rate sheet gives you a real baseline before you start shopping.

Why Your Credit Score and Loan Type Matter

Your credit score changes the math significantly. Borrowers with excellent credit—760 and above—may find that banks are genuinely competitive because banks have lower risk-based pricing for top-tier borrowers and may offer relationship discounts that close the gap. Borrowers in the 700–759 range typically see a clearer broker advantage because wholesale lenders price this tier more aggressively than retail banks.

Loan type matters just as much. Jumbo loans, investment properties, and non-QM loans almost always favor brokers because of product availability—banks simply don’t offer many of these products. FHA loans and VA loans may favor banks if you’re an existing customer with relationship discounts and streamlined processing. Conventional conforming loans are where the comparison is most competitive—and where shopping multiple lenders matters most.

A 0.25% rate difference on a $400,000 loan costs you $50/month or $18,000 over 30 years. On a $600,000 loan—common in Trophy Club, Southlake, or Westlake—that same 0.25% difference is $27,000 over 30 years. This is why shopping multiple lenders (both brokers and banks) is worth the effort. You’re not saving a few hundred dollars. You’re potentially saving tens of thousands.

Ready to see what rates you actually qualify for? Getting pre-qualified and compare rates from a broker who accesses multiple lenders is the fastest way to understand your real options—not the advertised rate, but the rate you’ll actually be offered based on your credit, income, and loan type.

Get Pre-Qualified TodayThe Real Cost Breakdown: Fees, Points, and Hidden Expenses

Rate is only part of the story. The full cost of a mortgage includes origination fees, discount points, lender credits, and third-party costs—and these vary significantly between lenders and channels. Borrowers who focus only on the interest rate and ignore closing costs often end up paying more than they expected, or more than they needed to.

Here’s what most people don’t realize: two lenders can quote you the exact same interest rate but have closing costs that differ by $3,000–$5,000. That difference doesn’t show up in the rate comparison—it shows up on closing day. This is why comparing Loan Estimates, not just rate quotes, is the only way to make an apples-to-apples comparison.

Origination Fees and Discount Points

Origination fees are what the lender charges to process your loan. Brokers typically charge 0.5% to 1.5% of the loan amount; banks typically charge 0.5% to 1.0%. On a $500,000 loan, that’s a range of $2,500 to $7,500 for brokers and $2,500 to $5,000 for banks. The difference can be significant—but it has to be weighed against the rate difference.

Discount points are pre-paid interest that buy down your rate. One point equals 1% of the loan amount and typically reduces your rate by 0.125% to 0.25%. Both brokers and banks offer discount points, but they’re priced differently. A 2-1 buydown loan is a specific structure that reduces your rate in the first two years—worth exploring if you’re buying in a higher-rate environment and expect rates to fall.

Lender credits work in the opposite direction—the lender gives you money to offset closing costs in exchange for a slightly higher rate. These are more common in the broker channel because brokers have more flexibility to structure the deal. If you’re short on cash at closing, lender credits can be a meaningful tool.

Yield Spread Premium (YSP) Explained

YSP is compensation brokers receive from wholesale lenders when they deliver a loan at a rate above the wholesale par rate. In plain terms: if the wholesale lender’s par rate is 6.75% and the broker delivers your loan at 7.00%, the lender pays the broker a percentage of the loan amount as compensation for that 0.25% rate premium you’re paying.

YSP is disclosed on your Loan Estimate and is not inherently deceptive—it’s standard practice and has been regulated by the CFPB since 2011. What matters is whether the total cost (rate plus fees) is competitive compared to other lenders. A broker earning YSP might still offer you a better deal than a bank charging a higher origination fee with a similar rate. Always compare total cost across lenders, not YSP in isolation.

YSP is compensation brokers receive from lenders when you accept a rate above the wholesale par rate. It’s disclosed and not inherently bad—it just means you’re paying a higher rate, which the broker is compensated for. The key question is whether the total cost (rate + fees) is still better than what banks are offering. Always compare the full Loan Estimate, not just one line item.

Third-Party Costs and Lender Credits

Appraisal, title, escrow, and survey fees are largely independent of whether you use a broker or a bank—they’re determined by third-party service providers. However, some lenders offer credits to offset these costs, and others don’t. This can swing your total closing costs by $1,000–$3,000 depending on the lender and the deal structure.

Texas-specific costs add another layer of complexity. Property tax escrow is required by most lenders, and in high-value areas like Southlake, Westlake, or Colleyville—where property taxes can run $12,000–$20,000 annually—the escrow requirement significantly affects your monthly payment and cash needed at closing. Homestead exemption timing also matters: if you close in the second half of the year, your first-year property tax may be higher than expected because the exemption hasn’t been applied yet. Some lenders explain this clearly; others don’t. Ask.

Product Availability: What Can You Get From a Broker vs a Bank?

For many borrowers, this is where the broker vs bank comparison stops being theoretical and becomes urgent. Rate differences matter. But if a bank can’t offer you the loan you need, the rate comparison is irrelevant. Product availability is where brokers have the clearest, most consistent advantage—and where the wrong choice can mean the difference between getting a loan and not getting one at all.

If you’re self-employed, an investor, have non-traditional income, or need a loan above conforming limits, you need to explore mortgage options for your situation with a broker who understands your specific needs. The standard bank menu may not have what you need.

Loans Brokers Can Access That Banks Can’t

The broker channel is where non-standard borrowers find solutions. Here’s what that looks like in practice:

- Non-QM loans: For borrowers who don’t fit the standard lending boxes—recent credit events, non-traditional employment, or complex financial structures. Learn more about non-QM loan options that brokers can access.

- Bank statement loans: For self-employed borrowers with strong bank accounts but inconsistent W-2 income. Explore self-employed mortgage loans designed for business owners and freelancers.

- DSCR loans: For real estate investors who qualify based on the property’s cash flow rather than personal income. If you’re building a portfolio in DFW, this is a critical product.

- Portfolio loans: Held by private lenders or credit unions, these don’t have to conform to Fannie Mae/Freddie Mac guidelines and can accommodate unusual situations.

- Private money loans: For investors or borrowers who need speed and flexibility over rate. Private money lending fills gaps that conventional channels can’t.

Loans Banks Excel At

Banks aren’t without their strengths. For the right borrower profile, bank products are genuinely competitive:

- Standard conforming loans: Fannie Mae and Freddie Mac-backed loans with the most competitive pricing for borrowers who fit the standard box. A fixed-rate mortgage on a conforming loan is where banks are most competitive.

- Jumbo loans for existing customers: Major banks like Chase and Bank of America offer relationship discounts on jumbo products for customers with significant deposits or investment accounts.

- FHA and VA loans: Banks with high volume in government-backed lending may offer streamlined processing and competitive pricing for existing customers.

- HELOC products: Banks often have competitive home equity line of credit products for existing mortgage customers.

- Private banking programs: For high-net-worth borrowers with $500,000+ in assets at the bank, private banking mortgage programs can offer rates and terms that brokers can’t match.

If you’re self-employed, an investor, or have non-traditional income, that’s exactly what brokers are designed to handle. A free consultation can help you understand which loan products you qualify for—and whether the broker channel opens doors that banks have closed.

Explore Your Loan OptionsSpeed and Service: Closing Timeline and Customer Experience

One of the most persistent myths in mortgage lending is that banks close faster. The reasoning sounds intuitive: banks have everything in-house, so the process must be more streamlined. The reality is more complicated—and the data doesn’t support the myth.

Average closing times for both brokers and banks in 2025 data fall in the same range: 30–45 days from application to close. There is no statistically significant difference in closing timelines between the two channels when you control for loan complexity. What drives closing speed is the specific lender’s underwriting capacity, your responsiveness as a borrower, and the appraisal timeline—not whether you went to a broker or a bank.

Both brokers and banks close in 30–45 days on average. Speed depends on the specific lender, your responsiveness, and the appraisal timeline—not whether you go to a bank or broker. Don’t sacrifice a better rate for perceived speed that doesn’t actually exist in the data. A 0.25% rate difference costs you $18,000 over 30 years. A few extra days to close costs you nothing.

Broker Processing: Myth vs Reality

The myth that brokers are slower stems from the idea that adding an intermediary adds time. In practice, the opposite can be true for complex loans. A broker can submit your application to multiple wholesale lenders simultaneously, which means if one lender has a backlog or raises a concern, the broker can pivot to another lender without starting over. That flexibility can actually speed up complex transactions.

Broker processing speed is determined by the wholesale lender’s underwriting capacity, not the broker’s. And brokers have a strong financial incentive to close quickly—they don’t get paid until the loan closes. That alignment of incentives matters.

Bank Processing: Advantages and Limitations

Banks with fully in-house processing can close simple loans in 25–35 days when everything goes smoothly. For a borrower with a straightforward financial situation, strong credit, and an existing banking relationship, this streamlined process is a real advantage. Banks also tend to have more consistent underwriting standards because they’re applying their own guidelines rather than wholesale lender guidelines that can vary.

The limitation is volume. When banks are busy—particularly during DFW’s spring peak season from March through June—underwriting queues can stretch closing timelines just as much as any broker’s wholesale lender. Banks may also require more documentation upfront for certain loan types, which can slow the process if you’re not prepared.

Transparency and Accountability: How Are They Compensated?

This section makes some people uncomfortable, but it shouldn’t. Understanding how your lender gets paid is one of the most important things you can do as a borrower. Both channels have compensation structures that create potential conflicts of interest—but only one of them is required to disclose those conflicts to you.

The CFPB requires brokers to disclose their compensation on the Loan Estimate within three business days of application. You can see exactly what the broker is earning from the lender and/or from you. That transparency is powerful. When you understand your loan estimate and closing disclosure, you can evaluate whether the broker’s compensation is reasonable relative to the rate and terms you’re receiving.

Broker Compensation: Yield Spread Premium and Broker Fees

Brokers can be compensated in three ways: by the lender only (YSP), by the borrower only (broker fee), or by both—though CFPB rules limit the total compensation structure. The key point is that all of it is disclosed. You see it on your Loan Estimate. You can ask questions about it. You can negotiate.

Typical broker compensation ranges from 0.5% to 2.0% of the loan amount, with 1.0% to 1.5% being most common. On a $500,000 loan, that’s $5,000–$7,500. Whether that’s worth it depends entirely on whether the broker’s access to wholesale pricing and specialized products saves you more than that compensation costs. In most cases for non-standard borrowers, it does. For standard borrowers, it’s a closer call—which is why you compare.

Bank Loan Officer Compensation: Hidden Incentives

Bank loan officers are typically salaried with commission based on loan volume or margin. Here’s what most borrowers don’t realize: that commission structure is not disclosed to you. It’s an internal bank matter. You cannot see what the loan officer earns on your transaction, which means you cannot evaluate whether their incentive to offer you a higher rate is affecting the quote you received.

Higher margin—meaning a higher rate relative to the bank’s cost of funds—typically means higher commission for the loan officer. This creates an incentive to offer you a rate that’s higher than necessary. Bank loan officers are required to offer the best cost option available to that borrower, but “best cost” is defined within the bank’s product menu, not across the market. The conflict of interest exists; it’s just hidden rather than disclosed.

The takeaway here isn’t that bank loan officers are dishonest—most aren’t. It’s that the disclosure framework for brokers actually gives you more information to work with, not less. Transparency is a feature, not a warning sign.

Regulatory Oversight and Consumer Protections in Texas

Both mortgage brokers and bank loan officers operate within a regulated framework in Texas, but the oversight structure is different—and knowing the difference helps you understand your recourse if something goes wrong.

Mortgage brokers in Texas must be licensed by the Texas Department of Savings and Mortgage Lending (SML). Bank loan officers must be NMLS-registered but are regulated by the Office of the Comptroller of the Currency (OCC) or the Federal Reserve, depending on the bank’s charter. Both must comply with CFPB regulations and federal fair lending laws. The practical difference is where you file a complaint and what remedies are available.

Verifying Licenses and Credentials

Every mortgage broker and loan officer—regardless of channel—must have an NMLS license. Verifying this takes about two minutes and can save you from a significant problem. Go to nmlsconsumeraccess.org, search by name or NMLS number, and look for three things: active license status, no disciplinary actions or orders, and proper state endorsements for Texas.

Texas brokers should have both a broker entity license and individual MLO licenses for each loan officer in their office. If you can’t find a lender’s license or it shows inactive status, stop the conversation. Ask for NMLS numbers before you provide any personal financial information.

Filing Complaints and Seeking Recourse

If you have a complaint against a mortgage broker, file it with the Texas SML at mortgage.texas.gov. For national banks, complaints go to the OCC at occ.gov. For any lender, you can also file with the CFPB at consumerfinance.gov—the CFPB has authority over all mortgage lenders regardless of charter type.

Texas also provides additional protection through the Deceptive Trade Practices Act (DTPA), which allows borrowers to sue for deceptive practices in mortgage transactions and recover damages plus attorney fees. This is a meaningful protection that goes beyond federal remedies. Complaints should generally be filed within one to two years of the deceptive practice to preserve your rights.

It’s also worth noting that Texas has specific constitutional restrictions on cash-out refinancing under Article XVI, Section 50(a)(6). These restrictions apply to both broker-originated and bank-originated loans—the channel doesn’t change the rule. If you’re exploring a cash-out refinance in Texas, make sure your lender understands these requirements thoroughly.

DFW Market Context: Broker vs Bank Landscape in Your Area

The DFW metro is one of the most competitive mortgage markets in the country, and that competition works directly in your favor. With 200+ licensed mortgage brokers and 50+ direct bank lenders operating across Tarrant and Denton counties, borrowers in Trophy Club, Grapevine, Roanoke, Keller, Argyle, Colleyville, Southlake, and Westlake have genuine leverage in the lending process.

DFW’s population growth—running at approximately 2.5% annually and adding over 150,000 residents per year—drives consistent mortgage demand that keeps lenders competing aggressively for business. That competition translates to better pricing, more flexible underwriting, and lenders who are motivated to close your loan efficiently.

Median home prices in the communities served by local brokers tell an important story about product needs. Trophy Club and Westlake median prices have been running $600,000–$1.2M+, Southlake and Colleyville in the $700,000–$1.5M range, and even Grapevine and Roanoke have seen significant appreciation into the $450,000–$700,000 range. These price points push many transactions above conforming loan limits, which makes broker access to jumbo loan products particularly valuable in this market.

Broker Presence in DFW

Independent and small-chain mortgage brokers are well-established in the DFW market, with strong specialization in jumbo loans, investment properties, and non-QM products. Local brokers who have built relationships with 50–100+ wholesale lenders can shop your loan across a wide range of pricing and product options in a single business day. That breadth is particularly valuable in a market where loan amounts frequently exceed conforming limits and borrower profiles often include self-employment, investment income, or complex financial structures.

Broker competition in DFW is strong enough that borrowers can negotiate compensation. If a broker’s fee seems high relative to the rate improvement they’re offering, say so. In a competitive market, brokers have incentive to be flexible.

Bank Direct Presence in DFW

Major national banks—Chase, Bank of America, Wells Fargo, Citi—all have active DFW mortgage divisions with loan officers who understand the local market. Regional banks like Comerica, Prosperity Bank, and Texas Capital Bank offer competitive products with a local relationship focus. Credit unions serving DFW—including some of the largest in Texas—offer a third channel with member benefits and unique portfolio products that don’t fit neatly into either the broker or bank category.

Bank pricing in DFW is competitive but less transparent than broker pricing. You can get a rate quote from a bank, but you won’t see their cost of funds or margin the way you can see a broker’s compensation on a Loan Estimate. That asymmetry is why comparison shopping matters so much in this market.

Seasonal patterns in DFW mortgage demand peak from March through June, when purchase activity is highest. During peak season, both brokers and banks can see extended underwriting timelines due to volume. If you’re buying in spring, start the pre-qualification process early and be responsive with documentation to avoid delays. To get a quote from a DFW mortgage broker who knows the local market, starting early gives you the most leverage.

How to Shop and Compare: The Right Way to Get the Best Deal

Everything in this guide comes down to one action: comparison shopping. The data is unambiguous. CFPB research shows that borrowers who get three to five quotes save an average of 0.25% to 0.375% on their rate compared to those who get only one or two quotes. On a $400,000 loan, that’s $18,000–$27,000 over 30 years. On a $600,000 loan in Trophy Club or Southlake, it’s $27,000–$40,500. The time investment is two to three hours. The return is extraordinary.

Here’s how to do it right.

Pre-Qualification vs Pre-Approval: What’s the Difference?

Pre-qualification is a quick estimate based on self-reported information. No documentation required, no hard credit inquiry, and it gives you a rough sense of what you might qualify for. Use pre-qualification to compare rates across multiple lenders without triggering multiple hard inquiries on your credit report.

Pre-approval is a verified approval based on actual documentation—credit check, income verification, asset verification. It’s what sellers and agents take seriously when you make an offer. Get pre-qualified with multiple lenders first to narrow your options, then get pre-approved with your top two or three choices before you make an offer on a home. The credit inquiry impact from multiple mortgage applications within a 14–45 day window is minimal—credit scoring models treat them as a single inquiry when you’re rate shopping.

Reading and Comparing Loan Estimates

The Loan Estimate is the most important document in the mortgage process. It shows you the rate, points, origination fee, third-party costs, and lender compensation—all on a standardized form that makes comparison possible. Request Loan Estimates from all lenders on the same day, because rates change daily and a quote from Monday compared to a quote from Friday is not an apples-to-apples comparison.

When comparing Loan Estimates, focus on three numbers: the interest rate, the total origination charges (Section A), and the total closing costs. Don’t get distracted by individual line items. Ask each lender about lender credits and rate buydowns—these can significantly reduce upfront costs, and not every lender volunteers this information proactively. Exploring all available loan options before you commit to a lender ensures you’re not missing a structure that could save you money.

Don’t lock your rate until you’ve compared all your options and understand the total cost. Rate locks typically last 30–60 days, and locking too early can cost you if rates drop before closing.

Red Flags to Watch For

Most lenders are legitimate and professional. But there are warning signs that should make you pause:

- A lender who won’t provide a Loan Estimate within three business days of application—this is a federal requirement, not optional.

- Pressure to lock your rate immediately without giving you time to compare other options.

- Significant unexplained differences in closing costs between lenders that the lender won’t clarify.

- A loan officer who won’t explain their compensation structure or gets defensive when you ask.

- A lender whose NMLS license can’t be verified at nmlsconsumeraccess.org or shows inactive status or disciplinary actions.

Pre-qualify with at least 3 lenders—a mix of brokers and banks—within 2 weeks. Request Loan Estimates on the same day. Compare total closing costs, not just the rate. This takes 2–3 hours and can save you $10,000–$20,000. It’s the single best use of your time in the entire mortgage process, and it works regardless of which channel ultimately wins your business.

Start your rate comparison today. Start your mortgage application and rate comparison with a broker who accesses 50+ lenders and can show you options banks won’t offer—so you can compare those options against your bank’s best rate and make a truly informed decision.

Compare Rates From 50+ LendersMortgage Broker vs Bank Direct: The Verdict for Different Borrower Profiles

After all the data, all the comparisons, and all the nuance, here’s the practical synthesis: the right channel depends on who you are as a borrower. There’s no universal answer—but there are clear patterns that hold up across the data.

When Brokers Win

Brokers have a clear advantage in these situations:

- Self-employed borrowers with strong financials but inconsistent W-2 income. Banks require two years of tax returns and often can’t accommodate the complexity. Brokers access bank statement loans and non-QM products designed for this profile.

- Real estate investors needing DSCR loans or portfolio products. Most banks don’t offer DSCR loans at all, and those that do price them uncompetitively compared to wholesale lenders.

- Borrowers with non-traditional income—freelancers, commission-based earners, rental income, or complex financial structures. The standard bank underwriting box doesn’t fit, and brokers can find lenders who understand the profile.

- Jumbo loan borrowers without existing bank relationships. Wholesale jumbo pricing is often better than retail jumbo pricing, and brokers can shop multiple jumbo lenders simultaneously.

- Borrowers with fair credit (620–679) who need specialized lenders willing to work with their profile. Brokers have access to lenders who specialize in this credit range and price it more competitively than retail banks.

When Banks Win

Banks have a genuine advantage in these situations:

- Existing customers with relationship discounts. If you have $500,000+ in deposits or investments at a bank, their private banking mortgage program may offer rates and terms that wholesale pricing can’t match.

- Borrowers with excellent credit (760+) and simple financial situations. Banks price top-tier credit profiles very competitively, and their streamlined processing for straightforward loans can be a genuine advantage.

- Borrowers who value a single point of contact and in-house processing. Some borrowers prefer the simplicity of working with one institution that handles everything internally.

- Borrowers with existing deposits or investment accounts who qualify for portfolio discounts. Some banks will reduce your rate by 0.125%–0.25% if you maintain a certain balance with them.

When It’s a Wash (Shop Both)

For many borrowers, the channel doesn’t determine the winner—the comparison does:

- First-time homebuyers with good credit and standard financial situations. Both channels are competitive; the best rate comes from shopping.

- Borrowers with conforming loan amounts and standard loan types. The wholesale discount and broker compensation often roughly offset each other, making the comparison close.

- Borrowers with 20%+ down payment and strong credit. Both channels price this profile well; comparison shopping determines the winner.

The real winner in every scenario is the borrower who shops both channels. The channel is not the strategy. Comparison is the strategy.

“The best mortgage rate doesn’t come from the right channel. It comes from the right comparison. Borrowers who get three or more quotes consistently outperform those who accept the first offer—regardless of whether that first offer came from a broker or a bank.”

Frequently Asked Questions: Mortgage Broker vs Bank Direct

It depends on your specific situation, and there’s no single right answer for every borrower. Brokers typically offer better rates and more product options—especially for self-employed borrowers, real estate investors, and jumbo loan borrowers—because they access wholesale pricing across 50–100+ lenders. Banks may be competitive if you’re an existing customer with excellent credit, a simple financial situation, and significant assets at the bank that qualify you for relationship discounts. The real answer is to shop both channels: get quotes from at least one broker and at least two banks, compare the Loan Estimates on the same day, and let the numbers tell you which channel wins for your specific profile.

CFPB research shows that borrowers who get three to five quotes save an average of 0.25% to 0.375% on their rate compared to those who get only one or two quotes. On a $400,000 loan, that’s $50–$75 per month or $18,000–$27,000 over the life of a 30-year loan. On a $600,000 loan—common in communities like Trophy Club, Southlake, or Westlake—the savings range from $27,000 to $40,500. Freddie Mac research has consistently confirmed this finding across multiple market cycles. The time investment of two to three hours to gather and compare quotes is one of the highest-return activities in the entire home-buying process.

YSP is compensation that brokers receive from wholesale lenders when you accept a rate above the wholesale par rate—essentially, the lender pays the broker for delivering a loan at a higher rate than the minimum available. It’s disclosed on your Loan Estimate and is standard practice in the broker channel, regulated by the CFPB since 2011. YSP is not inherently bad or deceptive—it’s simply one component of the broker’s compensation structure. What matters is the total cost of the loan (rate plus all fees), not the YSP in isolation. If the broker’s total cost is still lower than the bank’s total cost, the YSP is irrelevant. Compare total closing costs across all lenders and negotiate if any component seems disproportionately high.

No—both brokers and banks close loans in the same average range of 30–45 days based on 2025 data. The “banks are faster” narrative is a persistent myth that doesn’t hold up when you look at actual closing timelines across channels. What determines closing speed is the specific lender’s underwriting capacity, your responsiveness as a borrower in providing documentation, and the appraisal timeline—none of which are channel-dependent. For complex loans, brokers can actually be faster because they can submit to multiple wholesale lenders simultaneously and pivot if one lender raises an issue. Don’t sacrifice a better rate for perceived speed that the data doesn’t support.

Yes, absolutely—but brokers are almost always your best option if your income doesn’t fit neatly into a W-2 box. Brokers access bank statement loans, non-QM loans, and specialized wholesale lenders who understand self-employed income structures, including business owners, freelancers, and commission-based earners. Banks typically require two years of tax returns and apply standard underwriting guidelines that can penalize self-employed borrowers who take legitimate deductions that reduce their reported income. A broker who specializes in self-employed borrowers can often find a loan product that accurately reflects your financial strength and gets you approved at a competitive rate. Getting pre-qualified with a broker who has experience with self-employed borrowers is the right first step.

Go to nmlsconsumeraccess.org and search for the broker’s or loan officer’s name or NMLS number—every licensed mortgage professional must have one. Look for three things: active license status (not expired or inactive), no disciplinary actions or regulatory orders, and proper state endorsements for Texas. Texas mortgage brokers should have both a broker entity license and individual MLO licenses for each loan officer in their office. If you can’t find a lender’s license or it shows any issues, stop the conversation immediately and do not provide personal financial information. This verification takes less than five minutes and is one of the most important steps in protecting yourself in the mortgage process.

Ready to Compare Mortgage Broker vs Bank Rates for Your DFW Home?

You now understand the real differences between mortgage brokers and banks—and you know that the best rate comes from shopping, not from the channel. The next step is to get actual quotes and see what you qualify for.

A broker who accesses multiple lenders can show you options banks won’t offer, and you can compare those options against your bank’s best rate. That’s how you win. Whether you’re buying in Trophy Club, Grapevine, Roanoke, Keller, Southlake, or anywhere across the DFW metro, the comparison process starts with one step.

Start your pre-qualification today and take control of your mortgage decision—with real numbers, not marketing claims.

Get Pre-Qualified and Compare Rates From 50+ LendersOasis Home Mortgage | 7 Greenbriar Ct, Trophy Club, TX 76262